This is Post 16 of 16 in the Taiwan Risk Series. Full series at polarismng.com

Consequence #8, 9 & 10 — The Long Game: Innovation Divorce, Nuclear Risk, and Why Taiwan Is Not Crimea

This final post covers the three consequences that do not fit neatly into GDP models. They are harder to quantify than a percentage contraction. They are not harder to understand.

The Innovation Divorce

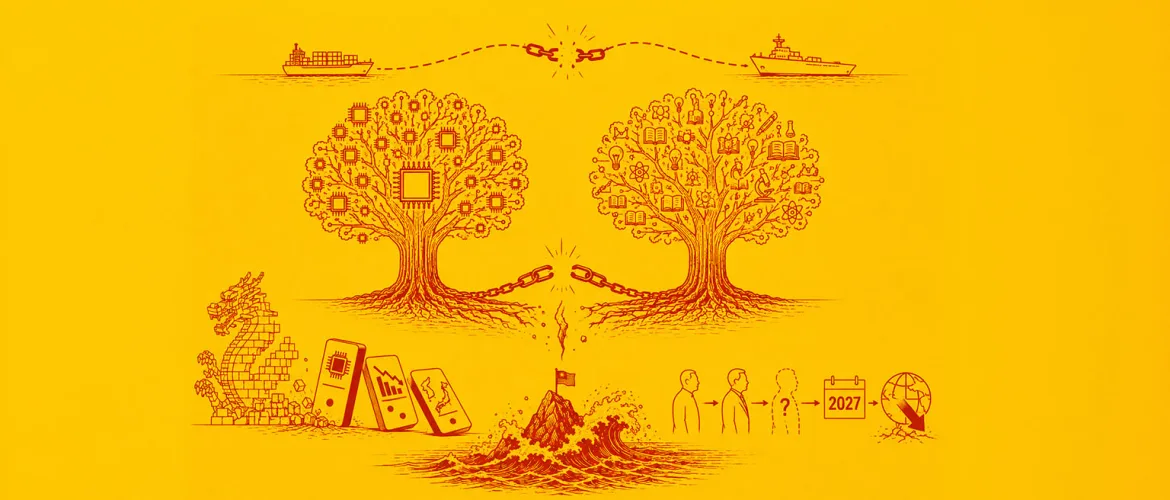

A severe and sustained US-China rupture — the kind that a Taiwan conflict would produce — would force two parallel innovation ecosystems. The world’s two largest scientific communities, which have collaborated, competed, and cross-pollinated for decades, would cease to function as a single knowledge system.

Chinese researchers in US universities would leave or be expelled. Joint ventures in AI, quantum computing, biotechnology, and clean energy — fields where collaboration has accelerated progress for both sides — would be unwound. The transfer of knowledge that has quietly driven much of the technology acceleration of the past twenty years would stop.

This is not a two-year disruption. It is a permanent bifurcation. The pace of innovation in every critical technology field would slow — not for one country, but for both, and therefore for the world.

The Nuclear Variable

A US-China conflict over Taiwan is not a conventional war between two non-nuclear powers. Both sides have nuclear arsenals. Both sides have doctrines that, under certain conditions, contemplate their use.

Analysts estimate the probability of tactical nuclear use in a US-China conflict over Taiwan at 5–8%. Strategic exchange: below 2%. Those numbers may sound small. Applied to a conflict involving the world’s two largest economies and two of its three largest nuclear arsenals, they represent consequences that no dashboard can adequately quantify.

This KPI does not have a traffic light. It is the reason all the other traffic lights matter.

Taiwan Is Not Crimea

The final consequence is the one most frequently misframed in public discourse. A Chinese seizure of Taiwan is sometimes discussed as if it might resemble Russia’s annexation of Crimea in 2014 — a rapid territorial transfer with limited resistance, absorbed as a fait accompli by the international community.

The evidence does not support that framing. Two-thirds of Taiwan’s population state they would actively resist invasion. Taiwan has a trained military, mountainous terrain, and urban geography designed — by history if not by planning — for defensive warfare. A Chinese occupation would face sustained guerrilla resistance in the world’s most semiconductor-dense island, with global media coverage and international support for the resistance.

This is not a Crimea scenario. This is an Afghanistan scenario — with semiconductors, nuclear weapons, and $5 trillion in annual maritime trade as the backdrop.

🔴 Innovation bifurcation: permanent, generational, unquantifiable in GDP terms

🔴 Nuclear escalation risk: 5–8% (tactical), <2% (strategic) — both numbers are material at civilisational scale

🔴 Occupation resistance: Taiwan is not Crimea — plan for a decade-long conflict, not a week-long fait accompli

What This Series Was For

The purpose of a risk dashboard is not to predict an event. It is to ensure you are not surprised by one.

Over 16 posts, we have walked through 10 KPIs with quantified thresholds and 6 posts on consequences that together represent the largest potential economic shock in modern history. The overall dashboard reading as of May 2026 is 🟡 Amber. One KPI is in the red zone. The peak risk window remains 2027–2029.

The question to ask is not “will this happen?” It is: what is our plan if three more KPIs turn red before 2028?

At Polaris, this is the kind of strategic risk work we build for clients who cannot afford to be reactive. If your business has material exposure to Asia-Pacific geopolitical risk and you would like to discuss a tailored monitoring framework, we would be glad to talk.

Sources across this series: Bloomberg Economics (Feb 2026), ODNI Annual Threat Assessment (March 2026), Janes Defence Intelligence (July 2025), RAND Corporation, Polymarket ($31.4M traded, May 2026), Manifold Markets, Stimson Center, Global Guardian, AEI, Responsible Statecraft, US DoD Pentagon Report 2025, China Leadership Monitor, The Diplomat.

© Polaris Management SL — polarismng.com

Leave A Comment